Growing partnerships across Michigan through shared services to help strengthen Community Banks

Mackinac Credit + Compliance (MCC) was formed in 2022 as a co-sourcing partner offering credit, compliance and operational consulting services to support community banks. Founded by former mBank executives who led that institution through both organic and external growth to $1.5 billion in assets, MCC now works alongside community banks across Michigan to provide seasoned support that strengthens day-to-day operations and keeps institutions aligned with regulatory expectations. “We’ve been in their shoes,” says Tammy McDowell, MCC President and Co-Founder. “We know what it’s like to juggle roles and stretch a small team. That’s why we built MCC: to meet banks where they are and help them stay competitive and grow.

From Bank Leaders to Trusted Partners

When MCC launched in 2022, the market was still rebuilding after the pandemic. Commercial loan demand had slowed down, and many institutions were taking a cautious approach to hiring and investment. But as conditions began to improve, institutions started revisiting their growth strategies, exploring mergers and acquisitions and becoming more open to trusted outside support. “When we organized MCC after the sale of mBank, we anticipated that community banks would face a shifting landscape post-COVID,” said Paul Tobias, MCC Board Member and past Chairman of mBank. “To stay competitive, banks would need support meeting regulatory expectations while also focusing on efficiency and shareholder value. MCC was built to complement internal resources by offering experienced professionals who can step in and support both day-to-day operations and long-term strategy.”

From Bank Leaders to Trusted Partners

When MCC launched in 2022, the market was still rebuilding after the pandemic. Commercial loan demand had slowed down, and many institutions were taking a cautious approach to hiring and investment. But as conditions began to improve, institutions started revisiting their growth strategies, exploring mergers and acquisitions and becoming more open to trusted outside support. “When we organized MCC after the sale of mBank, we anticipated that community banks would face a shifting landscape post-COVID,” said Paul Tobias, MCC Board Member and past Chairman of mBank. “To stay competitive, banks would need support meeting regulatory expectations while also focusing on efficiency and shareholder value. MCC was built to complement internal resources by offering experienced professionals who can step in and support both day-to-day operations and long-term strategy.”

Co-sourcing was a newer concept for many institutions within the traditional in-house credit administration and compliance areas of the bank. But over time, those initial reservations have turned into repeat engagements and further operational support in other departments. Kelly George, CEO & Co-Founder, explains, “We partner with community banks of all sizes — from several billion dollars of assets to less than a hundred million, both well-established with long legacies and newer institutions that have formed in the state over the past few years. We have a large bandwidth of services pending the scope and scale of the banks’ needs to tailor solutions and are not a one-size-fits-all company. Every community bank is as unique as the markets it serves, and we understand that well.” That was the case at Shelby State Bank.

The Right Help, Right When You Need It

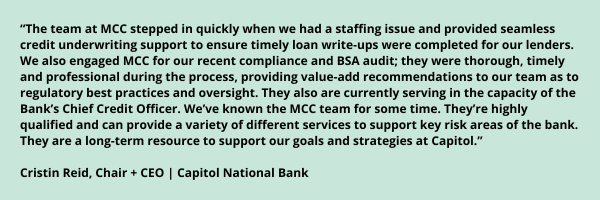

Flexibility and simplicity are baked into MCC’s business model. Their core services cover three areas. On the commercial credit side: underwriting, loan processing & typing, annual internal loan reviews, appraisal reviews, CECL assistance and a variety of other credit administrative services. MCC can also serve in the capacity of Chief Credit Officer for those organizations needing executive-level support. Compliance oversight services include audits, risk assessments, policy development and BSA/AML reviews. For institutions needing comprehensive support, MCC also serves in the role of Senior Compliance Officer, led by 35-year FDIC veteran Scott Alexander, MCC SVP and Director of Compliance. Rounding it out, MCC offers a variety of consulting services such as external loan reviews, M&A due diligence, examination preparation and guidance, CRE policy guidance and comprehensive board reporting. “This level of support is especially impactful in smaller communities where procuring talent can be more challenging,” Alexander explains. “A lot of these banks just don’t have ac[1]cess to the skills and expertise they need. We’re able to bring a higher level of experience to them and we do it in a way that feels collaborative, not intrusive. We are there to be a value-added partner.” Capitol National Bank is one of many that’s experienced this value firsthand.

The Future Is Bright for Community Banks

George sees MCC’s role as part of a much broader story. “The Michigan community banking ecology remains strong, and community banks are the primary conduit for many of the state’s more rural markets in terms of capital needed for economic development and job growth. That’s why it is so vital that they remain financially healthy, nimble and operationally well-positioned. We can help strengthen internal talent gaps and risk oversight needs to ensure they remain highly competitive and an integral part of the communities they serve.” For McDowell, the best part is the trust they’ve built with clients in just three years. “We started from zero and now serve many banks across Michigan and various other states. We’ve grown not because we shouted the loudest, but because our clients kept telling others about what we delivered. We are grateful for their continued support of MCC and the confidence they place in our team.” In an industry that values word-of-mouth referrals above all, that’s saying something.

This article first appeared in Community Bankers of Michigan’s magazine, Community Spirit, in June 2025.

If you’d like more information about MCC, please visit their website.